Forterra Inc. (NASDAQ: FRTA) is a leading manufacturer of water and drainage pipe & products for a variety of water-related infrastructure applications. Based in Irving, Texas, it employs more than 5,500 people and operates 101 facilities, with products available throughout the U.S. and Eastern Canada.

On November 8th, the company announced results for the quarter ended September 30, 2017. During the quarter, Forterra faced several operational issues (Including hurricanes Harvey and Irma) that adversely impacted its performance. The company also closed the sale of its U.S. concrete and steel pressure-pipe business during the quarter. That divestiture reduced sales by $8.9 million, and the company recorded a $31.6 million loss on that transaction, which is what pulled it into the red.

Notwithstanding the quarterly performance, FRTA shares were up 76% over the last few trading sessions. Trading volume has been brisk.

While these factors created headwinds for the company this year, FRTA’s demand outlook remains favorable against the backdrop of healthy economic fundamentals. Expectations were continued in residential housing growth and improving funding initiatives to support highway infrastructure projects. The backlog in the water and drainage segments remained solid and Supports Company’s outlook for the longer-term growth.

If we factor in all these headwinds, Forterra reported a reasonable set of numbers. Third quarter 2017 net sales increased to $444.3 million, compared to $441.1 million in the prior-year quarter. Net loss for the quarter was $11.5 million, or a loss of $0.18 per share, compared to net income of $8.4 million, or $0.19 per share, in the prior-year quarter.

The results demonstrate the company’s ability to successfully execute on multiple objectives on a sequential quarter basis, including higher selling prices, lower costs, and improved earnings. Additionally, despite the impact of two major hurricanes, Adjusted EBITDA was above the mid-point of its guidance range.

Moving forward, the company continues to expect to see increasing highway infrastructure spending and deployment of FAST act dollars as it heads into 2018. The management believes that the fundamental need for infrastructure investment in the U.S. including both highway and municipal water projects is greater than ever.

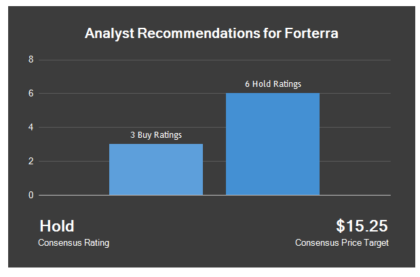

Therefore, the company has significant opportunities to enhance earnings in 2018 and beyond, with the divestiture of the U.S. concrete and steel pressure pipe assets, procurement initiatives, SG&A cost savings initiatives and corporate cost reductions all support expectations for a significant improvement in 2018. Driven by abovementioned factors, several equities research analysts recently issued favorable reports on EARS shares. On average, the consensus target is $15.25 over the medium term.

Source: dispatchtribunal.

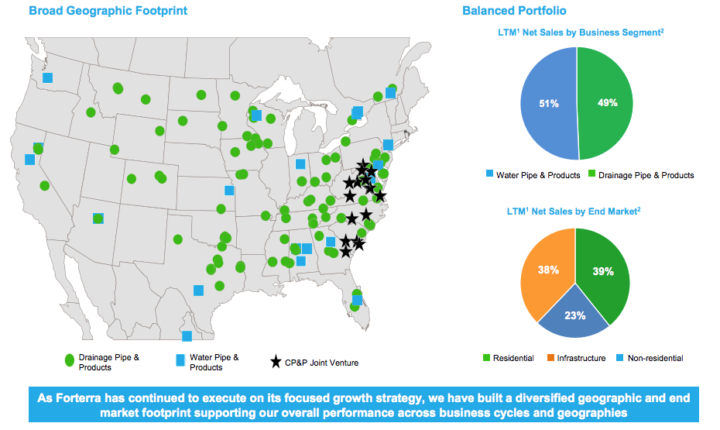

About the company: Forterra is a leading manufacturer of water and drainage pipe and products in the U.S. and Eastern Canada for a variety of water-related infrastructure applications, including water transmission, distribution, drainage, and storm water management.

Based in Irving, Texas, Forterra’s product breadth and significant scale help make it a one-stop shop for water-related pipe and products, and a preferred supplier to a wide variety of customers, including contractors, distributors, and municipalities.

Product Profile: The Company has a national Scale with Diversified Exposure Across Products and End Markets.

The outlook for the near term:

- The guidance range assumes a year over year decline in sales, including a $27 million reduction associated with the divestiture of the U.S. concrete and steel pressure pipe assets. Incorporating the impact of the divestiture, the high end of the guidance range assumes flat sales for the quarter while the low end conservatively implies a more significant decline.

- The guidance range anticipates delivering an improved year over year Adjusted EBITDA margin variance in Q4 2017 as compared to the prior quarter

- Net loss for the fourth quarter of 2017 is expected to range from $16 million to $13 million and Adjusted EBITDA expected to range from $20 million to $25 million

Management’s preliminary Thoughts on 2018

The management expect to see continued improvement in year over year results in 2018 reflecting the anticipated benefit of:

- Higher expected average selling prices

- Input cost inflation mitigated through the procurement initiatives

- Lower operating costs in Drainage resulting from the reorganization

- Lower corporate costs due to lower professional fees and other G&A cost savings initiatives

Industry overview and market opportunity for the company:

- The U.S. market size for drainage and water transmission pipes is estimated to be $20 billion by 2020, representing 7-8% per year growth

- Over 40% of infrastructure spend is on highway and street, water supply and waste water projects

- Expect to see the benefit of accelerating pace of Fixing America’s Surface Transportation Act (“FAST Act”) spending

- Underinvestment in municipal water infrastructure supports longer-term expectations for demand growth

- Outlook for single-family housing starts by state shows high single-digit to double-digit growth in 2017 in large states where Forterra has a significant presence including California, Pennsylvania, Florida, Georgia and Texas

- ~ 30% of commercial construction spending is driven by new construction starts – expect to see continued stable growth during the more mature phase of expansion in the current economic recovery cycle

2nd Quarter 2017 Financial Results:

Revenue and Profitability:

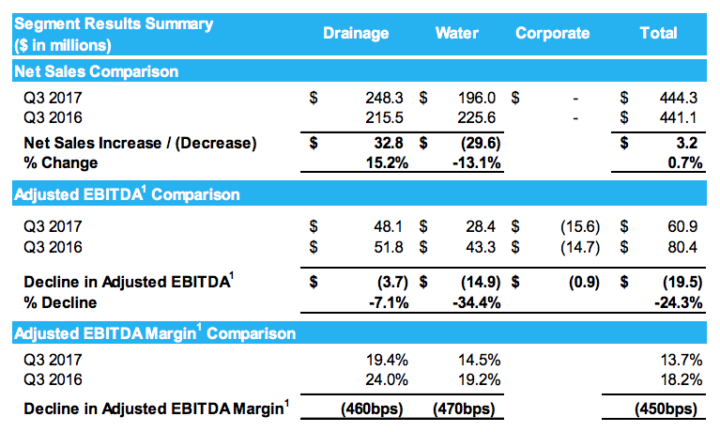

- Third quarter 2017 net sales increased to $444.3 million, compared to $441.1 million in the prior-year quarter.

- Net loss for the quarter was $11.5 million, or a loss of $0.18 per share, compared to net income of $8.4 million, or $0.19 per share, in the prior-year quarter.

- Adjusted EBITDA for the third quarter was $60.9 million, compared to $80.4 million in the prior-year quarter. The estimated Adjusted EBITDA impact of Hurricanes Harvey and Irma was approximately $3.7 million including a $3.0 million impact to Drainage Pipe & Products (“Drainage”) and $0.7 million impact to Water Pipe & Products (“Water”).

Liquidity:

- At September 30, 2017, the Company had cash of $41.1 million and outstanding debt on its senior term loan of $1.2 billion. As of September 30, 2017, there was no outstanding balance on the Company’s $300 million Revolver following an $80 million net pay down during the quarter.

- The Company expects to continue to build its cash position through the end of 2017 reflecting the anticipated benefit of positive cash flow from working capital during the fourth quarter.

Key risk factors and potential stock drivers:

- The working capital requirement is relatively large, as is inherent in this industry. Sustained efficient working capital management as the business grows, would be a key sensitivity factor for the company.

- The financial risk profile should improve supported by better working capital management, monetization of non-core assets, and improving cash accruals/profitability.

- Weakening of the financial risk profile due to slower than expected pace of operating performance improvement, or large, debt-funded capital expenditure could adversely affect the sentiments.

- Vulnerability to volatility in raw material prices is likely to persist over the medium term, given the limited flexibility to pass on price increases owing to competition.

- Also, the company is exposed to risk related to environment and adverse weather situations.

Stock Chart:

- On Monday, November 10th, 2017, FRTA was trading at $8.78 (+2.81%) on volume of 982K shares exchanging hands. Market capitalization is $570.34 million. The current RSI is 87.32

- In the past 52 weeks, shares of FRTA have traded as low as $3.02 and as high as $22.76

- At $8.78, shares of FRTA are trading above its 50-day moving average (MA) at $4.98 and below its 200-day MA at $10.96.

- The present support and resistance levels for the stock are at $8.11 & $9.03 respectively.

Welcome to Traders News Source

Our track record speaks for itself…

Traders News Source recent profiles and track record, 487% in verifiable potential gains for our members on 3 small cap alerts alone! These are just three examples from over two dozen winners this year.

January 31st, 2017 (NASDAQ: HIMX) opened at $5.10/share and hit a high of $9.68/share March 24th, 2017 for gains of 89% within 60 days- http://finance.yahoo.com/news/himax-technologies-review-4q-2016-130000319.html

May 23rd, 2016- (NYSE: XXII) opened at $.87/share hit a high of $3.03/share so far our member potential gains- 248% – http://mailchi.mp/tradersnewssource/updates-5-of-our-profiles-for-212-400-and-whats-coming-next?e=[UNIQID]

October 31st, 2017 (NASDAQ: PYDS) Although we have been covering this security for over a year, our recent coverage October 31st, 2017 opened at $1.45/share hit $4.10 within three days for gains of over 150%- http://mailchi.mp/tradersnewssource/update-pyds-back-in-the-value-zone-with-news-out?e=[UNIQID]

So, if you’ve been on the fence, perhaps it’s time to start doing some research and verify our numbers for yourself. We are constantly raising the bar and separate ourselves from the rest of the small-cap newsletters as the best in business.

We know with a large following comes a large responsibility as we have everyone from institutional investors to the beginner following our profiled securities in our newsletter. This is something we take very seriously always seeking small cap growth companies that have both near and long-term potential for our members.

Big Opportunities Trading Small Cap Stocks

***Get our small cap profiles, special situation and watch alerts in real time. We are now offering our VIP – SMS/text alert service for free, simply text the word “Traders” to the phone number “25827” from your cell phone***

Disclaimer

Traders News Source is a wholly owned subsidiary of Traders News Source LLC, herein referred to as TNS LLC.

Traders News Source has not been compensated for this report by anyone and the opinions if any are that of the author Vikas Agrawal, CFA. Author’s Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I, wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in the article.

This web site, published by TNS LLC, and is an investment newsletter that is built on the premise of assisting individual investors in learning about investing. Our goal as publishers of financial information is to provide research and analysis of investments to our subscribers. TNS LLC does not give buy or sell recommendations. We do purchase distribution rights from analyst, financial writers and bloggers for a fee that may be licensed to issue price targets and recommendations. Furthermore, we encourage you to speak to a licensed professional prior to making an investment in any type of publicly traded security.

We do sell advertising to other companies including brokerage firms, web sites, publicly traded issuers, investor relations firms, and investment publications, among others. TNS LLC makes no warranty as to the policies of these organizations, and in no way endorses their offers, services, or the content of their advertisements.

When an advertiser is a publicly traded company or a third party acting on behalf of a public company, we fully disclose all compensation in the email advertisement. Such disclosure is included in a disclosure statement in each of the advertisements sent via email.

17B Disclosure

Our reports/releases are a commercial advertisement and are for general information purposes ONLY. We are engaged in the business of marketing and advertising companies for monetary compensation. Never invest in any stock featured on our site or emails unless you can afford to lose your entire investment. The disclaimer is to be read and fully understood before using our services, joining our site or our email/blog list as well as any social networking platforms we may use.

PLEASE NOTE WELL: TNS LLC and its employees are not a Registered Investment Advisor, Broker Dealer or a member of any association for other research providers in any jurisdiction whatsoever.

Release of Liability: Through use of this website viewing or using you agree to hold TNS LLC, its operator’s owners and employees harmless and to completely release them from any and all liability due to any and all loss (monetary or otherwise), damage (monetary or otherwise), or injury (monetary or otherwise) that you may incur. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. TNS LLC encourages readers and investors to supplement the information in these reports with independent research and other professional advice. All information on featured companies is provided by the companies profiled, or is available from public sources and TNS LLC makes no representations, warranties or guarantees as to the accuracy or completeness of the disclosure by the profiled companies. None of the materials or advertisements herein constitute offers or solicitations to purchase or sell securities of the companies profiled herein and any decision to invest in any such company or other financial decisions should not be made based upon the information provide herein. Instead TNS LLC strongly urges you conduct a complete and independent investigation of the respective companies and consideration of all pertinent risks. Readers are advised to review SEC periodic reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D.

TNS LLC is compliant with the Can Spam Act of 2003. TNS LLC does not offer such advice or analysis, and TNS LLC further urges you to consult your own independent tax, business, financial and investment advisors. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s investment may be lost or impaired due to the speculative nature of the companies profiled.

The Private Securities Litigation Reform Act of 1995 provides investors a ‘safe harbor’ in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions or future events or performance are not statements of historical fact may be “forward looking statements”. Forward looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated. Forward looking statements in this action may be identified through use of words such as “projects”, “foresee”, “expects”, “will”, “anticipates”, “estimates”, “believes”, “understands”, or that by statements indicating certain actions & quote; “may”, “could”, or “might” occur.

Understand there is no guarantee past performance will be indicative of future results. In preparing this publication, TNS LLC has relied upon information supplied by its customers, publicly available information and press releases which it believes to be reliable; however, such reliability cannot be guaranteed. Investors should not rely on the information contained in this website. Rather, investors should use the information contained in this website as a starting point for doing additional independent research on the featured companies. The advertisements in this website are believed to be reliable, however, TNS LLC and its owners, affiliates, subsidiaries, officers, directors, representatives and agents disclaim any liability as to the completeness or accuracy of the information contained in any advertisement and for any omissions of materials facts from such advertisement. TNS LLC is not responsible for any claims made by the companies advertised herein, nor is TNS LLC responsible for any other promotional firm, its program or its structure.