Keryx Biopharmaceuticals, Inc. (NASDAQ: KERX), with headquarters in Boston, Massachusetts, is a commercial-stage company focused on bringing innovative medicines to people with renal disease. Keryx has programs underway to leverage its development and commercial infrastructure, including evaluation of ferric citrate as a treatment for iron deficiency anemia in adults with non-dialysis dependent chronic kidney disease (CKD) and in-licensing medicines for renal disease.

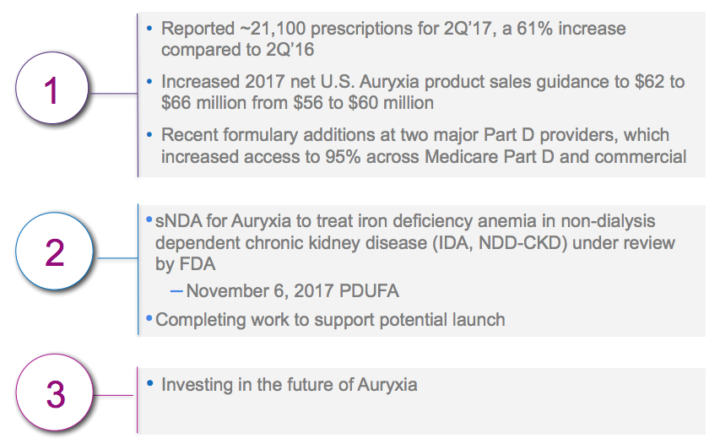

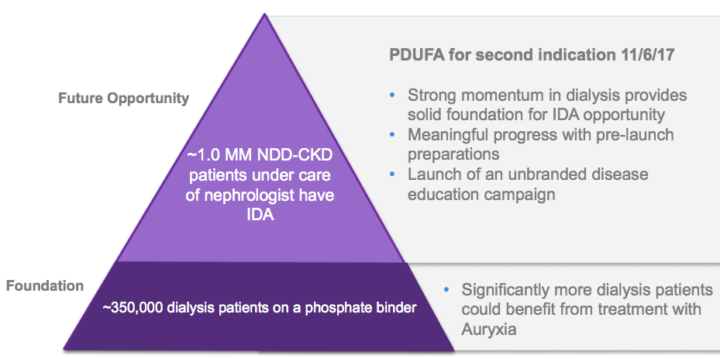

The company is poised for a Label Expansion Opportunity. A supplemental new drug application seeking approval of Auryxia for the treatment of patients with iron deficiency anemia and non-dialysis dependent CKD is currently under review, with a November 6, 2017, PDUFA action date. If approved for this indication, Keryx will have two indications for Auryxia to leverage its commercial infrastructure, as well as the broad patient access, familiarity and relationships established to date in treating hypophosphatemia.

The upcoming PDUFA action is likely to be one of the major near-term catalysts for the stock, as currently there is no FDA approved oral treatment to treat iron deficiency in non-dialysis-dependent chronic kidney disease. Therefore, KERX’s business risk profile is at a critical inflection point with a strong possibility to get the benefits of the catalyst.

The drug has already presented encouraging results in a pivotal Phase 3 trial where it showed statistically significant differences over placebo for the primary and secondary endpoints and potential FDA approval could help in expanding the addressable market for the drug as it will then be able to cover the NDD market, which consists of patients who are not yet required to be put on dialysis, or the stage which is referred to as End Stage Kidney Disease (ESKD).

Iron deficiency anemia is a severe disease and, today, as many as three out of four people with CKD and iron deficiency anemia are not being optimally treated with existing iron supplements. KERX is working diligently to ensure that they are prepared, pending FDA approval in early November, for a successful launch in this indication.

From a market size perspective, it is estimated that there are around 1.7 million NDD-CKD patients in the US itself. Out of these nearly 650,000 are being treated for iron deficiency anemia (IDA), presenting a significant untapped market for the drug, which is likely to be around $2.8 billion.

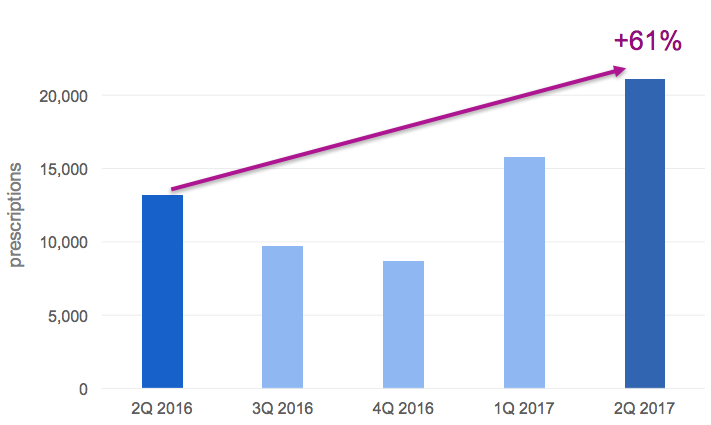

The company had recently announced its financial results for the quarter ended June 30, 2017. It also reviewed its commercial progress with Auryxia and upcoming milestones. Keryx reported second-quarter 2017 net U.S. Auryxia product sales of $14.1 million compared to $8.3 million in the second quarter of 2016, an increase of 71 percent.

The second quarter results reflect continued strength in Auryxia’s prescription demand. Increasing breadth and depth of prescribing among physicians primarily drove this demand. In fact, with this strong momentum, the company has increased its annual net Auryxia product sales guidance, reflecting improved confidence in its ability to bring this medicine to a greater number of people with chronic kidney disease (CKD) on dialysis this year.

Strong 2Q 2017 Auryxia Prescription Demand:

The management is extremely bullish about the opportunity to potentially add a second indication for Auryxia for the treatment of iron deficiency anemia in people with non-dialysis dependent chronic kidney disease. The progress that the company is making in dialysis coupled with the large opportunity to treat iron deficiency anemia form a solid basis for near to medium term.

Driven by the abovementioned factors, which are expected to translate into better business & financial performance for the drug in the coming months, Traders and investors seem to be pricing KERX positively. The stock currently has an average rating of “BUY” and a consensus price target of $9.50. Considering present valuation, KERX is at an extremely favorable risk-reward position.

Product/pipeline: Keryx developed and commercializes Auryxia® (ferric citrate), an iron-based phosphate binder, in the U.S. Ferric citrate is marketed as Riona® by Keryx’s Japanese partner, Japan Tobacco Inc. and Torii Pharmaceutical Co. Ltd. In September 2015, the European Commission granted European market authorization for Fexeric® (ferric citrate coordination complex).

Keryx has programs underway to leverage its development and commercial infrastructure, including evaluation of ferric citrate as a treatment for iron deficiency anemia in adults with non-dialysis dependent chronic kidney disease and in-licensing medicines for renal disease.

Recent business progress:

2017 Second quarter financial results:

The second quarter reflects strong demand and sales of Auryxia and therefore the management raised Auryxia’s 2017 net product sales guidance to $62 to $66 million. Additionally, the capital raised via the ATM strengthens its balance sheet and provides it with the financial flexibility/liquidity to continue to invest in business to support its anticipated growth appropriately.

Total revenues for the quarter ended June 30, 2017 were $15.1 million, compared with $9.3 million during the same period in 2016. Total revenues for the second quarter of 2017 include $14.1 million in net U.S. Auryxia product sales, compared to $8.3 million in the second quarter of 2016. Total revenues also include $1.0 million in license revenue during the second quarters of 2017 and 2016.

Research and development expenses for the quarter ended June 30, 2017 were $9.0 million, as compared to $7.0 million during the same period in 2016. The increase was primarily related to manufacturing and clinical activities to support the long-term growth of Auryxia.

Net loss for the quarter ended June 30, 2017 was $86.5 million, or $0.77 per share, compared to a net loss of $44.7 million, or $0.42 per share, for the comparable period in 2016. The increase in net loss is attributable to the recognition of $63.0 million of non-cash debt discount amortization related to the company’s outstanding convertible debt. This amortization expense is not expected to recur in future periods.

Cash and cash equivalents as of June 30, 2017 totalled $140.5 million compared to $111.8 million as of December 31, 2016.

2017 Financial Guidance:

Increased 2017 Auryxia guidance to $62 to $66 million, from $56 to $60 million, based upon:

- Strong 2Q prescription level and underlying demand

- Impact of broad formulary access: 95% of phosphate binder patients with Medicare Part D and commercial insurance now have unrestricted access.

- New range represents quarter-over-quarter growth for the remainder of 2017 of 25% to 35%

Key risk factors and potential stock drivers:

The company had been troubled by production issues, which impacted its revenue potential in negative ways in the past. Recurrence of any such exigencies would impinge the business risk profile of the company.

The upcoming catalyst of the FDA decision and continued improvement in drug distribution are expected to provide a boost to the stock to retain its momentum. Any adversities related with the same could upset the stock performance significantly.

KERX presently has net level losses. Therefore, any crunch in its liquidity and financial flexibility will further impact its business & financial profile.

Stock Chart:

On Tuesday, October 3rd, 2017, KERX closed at $7.19 on an average volume of 1.05 million shares exchanging hands. Market capitalization is $853.81 million. The current RSI is 51.82

In the past 52 weeks, shares of KERX have traded as low as $4.11 and as high as $8.38

At $7.19, shares of KERX are trading above its 50-day moving average (MA) at $7.04 and above its 200-day MA at $6.30

The present support and resistance levels for the stock are at $7.10 & $7.30 respectively.

Disclaimer

Traders News Source is a wholly owned subsidiary of Traders News Source LLC, herein referred to as TNS LLC.

Traders News Source has not been compensated for this report by anyone and the opinions if any are that of the author Vikas Agrawal, CFA. Author’s Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I, wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in the article.

This web site, published by TNS LLC, and is an investment newsletter that is built on the premise of assisting individual investors in learning about investing. Our goal as publishers of financial information is to provide research and analysis of investments to our subscribers. TNS LLC does not give buy or sell recommendations. We do purchase distribution rights from analyst, financial writers and bloggers for a fee that may be licensed to issue price targets and recommendations. Furthermore, we encourage you to speak to a licensed professional prior to making an investment in any type of publicly traded security.

We do sell advertising to other companies including brokerage firms, web sites, publicly traded issuers, investor relations firms, and investment publications, among others. TNS LLC makes no warranty as to the policies of these organizations, and in no way endorses their offers, services, or the content of their advertisements.

When an advertiser is a publicly traded company or a third party acting on behalf of a public company, we fully disclose all compensation in the email advertisement. Such disclosure is included in a disclosure statement in each of the advertisements sent via email.

17B Disclosure

Our reports/releases are a commercial advertisement and are for general information purposes ONLY. We are engaged in the business of marketing and advertising companies for monetary compensation. Never invest in any stock featured on our site or emails unless you can afford to lose your entire investment. The disclaimer is to be read and fully understood before using our services, joining our site or our email/blog list as well as any social networking platforms we may use.

PLEASE NOTE WELL: TNS LLC and its employees are not a Registered Investment Advisor, Broker Dealer or a member of any association for other research providers in any jurisdiction whatsoever.

Release of Liability: Through use of this website viewing or using you agree to hold TNS LLC, its operator’s owners and employees harmless and to completely release them from any and all liability due to any and all loss (monetary or otherwise), damage (monetary or otherwise), or injury (monetary or otherwise) that you may incur. The information contained herein is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. TNS LLC encourages readers and investors to supplement the information in these reports with independent research and other professional advice. All information on featured companies is provided by the companies profiled, or is available from public sources and TNS LLC makes no representations, warranties or guarantees as to the accuracy or completeness of the disclosure by the profiled companies. None of the materials or advertisements herein constitute offers or solicitations to purchase or sell securities of the companies profiled herein and any decision to invest in any such company or other financial decisions should not be made based upon the information provide herein. Instead TNS LLC strongly urges you conduct a complete and independent investigation of the respective companies and consideration of all pertinent risks. Readers are advised to review SEC periodic reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D.

TNS LLC is compliant with the Can Spam Act of 2003. TNS LLC does not offer such advice or analysis, and TNS LLC further urges you to consult your own independent tax, business, financial and investment advisors. Investing in micro-cap and growth securities is highly speculative and carries an extremely high degree of risk. It is possible that an investor’s investment may be lost or impaired due to the speculative nature of the companies profiled.

The Private Securities Litigation Reform Act of 1995 provides investors a ‘safe harbor’ in regard to forward-looking statements. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions or future events or performance are not statements of historical fact may be “forward looking statements”. Forward looking statements are based on expectations, estimates, and projections at the time the statements are made that involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated. Forward looking statements in this action may be identified through use of words such as “projects”, “foresee”, “expects”, “will”, “anticipates”, “estimates”, “believes”, “understands”, or that by statements indicating certain actions & quote; “may”, “could”, or “might” occur.

Understand there is no guarantee past performance will be indicative of future results. In preparing this publication, TNS LLC has relied upon information supplied by its customers, publicly available information and press releases which it believes to be reliable; however, such reliability cannot be guaranteed. Investors should not rely on the information contained in this website. Rather, investors should use the information contained in this website as a starting point for doing additional independent research on the featured companies. The advertisements in this website are believed to be reliable, however, TNS LLC and its owners, affiliates, subsidiaries, officers, directors, representatives and agents disclaim any liability as to the completeness or accuracy of the information contained in any advertisement and for any omissions of materials facts from such advertisement. TNS LLC is not responsible for any claims made by the companies advertised herein, nor is TNS LLC responsible for any other promotional firm, its program or its structure.